Beneteau: Record full-year earnings in 2023

Beneteau: Record full-year earnings in 2023

“2023 was a record year for Groupe Beneteau. The Group’s 8,000 staff achieved an outstanding collective performance: income from ordinary operations of over €240m, with a double-digit net margin. Our value-driven growth strategy is delivering a range of benefits; it is further strengthening the Group’s resilience and enabling it to position the Group’s operational profitability within a range that is significantly higher than its pre-Covid levels.

Its continued premiumization and its industrial agility will enable the Boat division to maintain an operating margin of 7% to 10% in 2024, despite the impact of higher interest rates on business.

This financial solidity confirms the Group’s strategy for product development and sustainable innovation, combined with growth in new services, such as digital and the sharing economy”, confirms Bruno Thivoyon, Groupe Beneteau Chief Executive Officer.

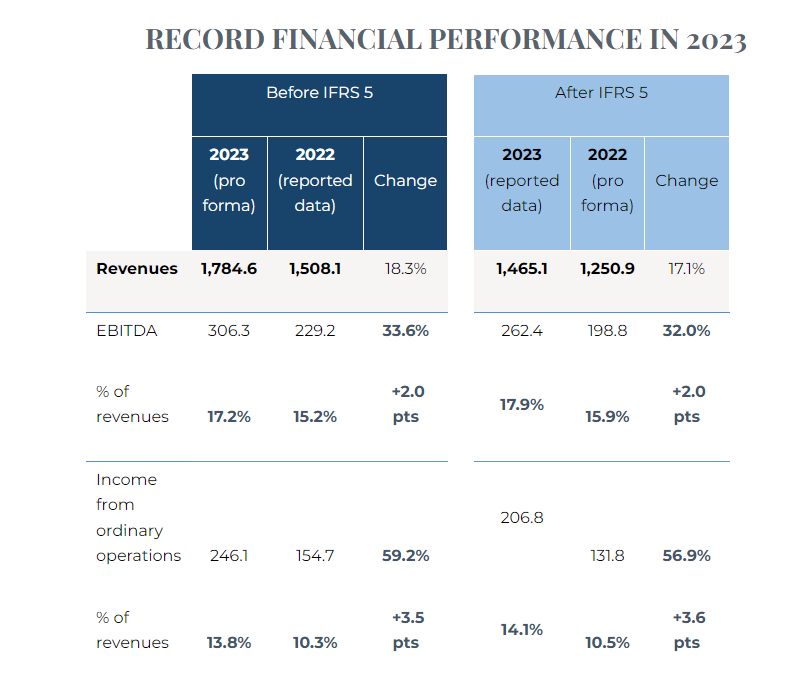

Following the announcement of the Housing division’s proposed sale, the Group’s key figures, before and after restatement linked to the application of IFRS 5[1], are presented below. The transaction is subject to approval by the French competition authorities, with their response expected during the first half of 2024.

Boat division: value-driven growth strategy delivering a range of benefits

As reported on February 12, the Boat division’s revenues came to €1,465m in 2023, up 17.1% from 2022 (+18% at constant exchange rates). The slowdown in demand for the Motor business (-€150m) was more than offset by the value-driven growth strategy across all the segments (+€190m) and the progress made with deliveries of sailing units (+€40m). Sales also benefited from the distribution network’s stock replenishment, back up to pre-Covid levels (+€150m), in a context of the normalization of sourcing conditions.

The Sailing business, with 31% full-year growth, was particularly dynamic, reflecting the significant upturn in sales to charter professionals (+68%), the commercial success of the new models released, and the Excess brand’s strong penetration on the catamaran market.

For the Motor business, up 9% at constant exchange rates, sales show strong growth for the Real Estate on the Water segments (+17%), thanks in particular to the commercial success of the PRESTIGE brand’s first catamaran models. The Dayboating segments recorded a 3% increase in revenues, with a 23% reduction in the number of units delivered. This benefited in particular from the extension of the Merry Fisher and Antares lines, as well as the launch of the DB range.

This excellent performance by the Boat division, outpacing the market on each segment, enabled it to achieve a record level of income from ordinary operations in 2023, up 57% from the previous year (€131.8m) to €206.8m, with an operating margin of over 14% of annual revenues, up €75m year-on-year.

The value creation strategy contributed €22m to this structural progress, while the progress made with operational performance levels represented a further improvement of €3m.

In addition, 2023 income benefited from the Group effectively anticipating the impacts of inflation (+€25m), as well as the stock replenishment seen across the distribution networks, back up to their pre-Covid levels in terms of volumes (+€44m).

Lastly, development costs linked to the new ERP totaled €13m for the year, up €6m from 2022, while the changes in €/$ exchange rates, which had exceptionally contributed to income in 2022, have since normalized (-€12m).

The Boat division’s EBITDA[2] is up 32% to €262.4m, representing 17.9% of revenues (vs. 15.9% in 2022), up 32%.

Housing division: continued profitable growth

Benefiting from the sustained trends seen on the camping tourism markets, the Housing division generated €319.6m of revenues in 2023, up 24% year-on-year. This growth, combined with excellent operational management, enabled the division to generate €39.3m of income from ordinary operations over the period, representing 12.3% of revenues, up 72% from 2022. In accordance with IFRS 5, this income is now recognized at Group net income level, after deducting taxes and other non-operating expenses.

Solid financial structure: 10.2% net income and €247m of net cash

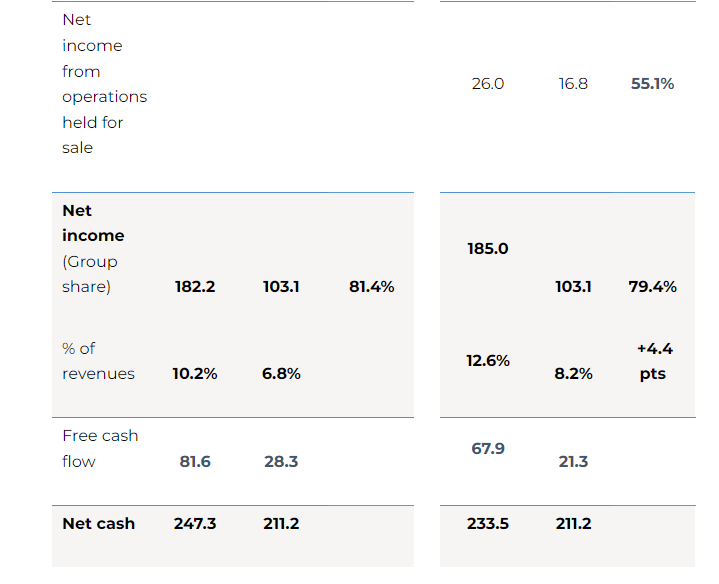

Net income (Group share) came to €185m for 2023, up 79% from 2022 (€103m). It includes €6.4m of financial income (vs. -€12.3m in 2022), benefiting from the change in interest rates, while the previous year was affected by currency hedging income and expenses (-€10m).

Over the year, the share of associates is up €2m, driven primarily by growth in the financing activities of its subsidiary SGB.

The Group’s free cash flow before IFRS 5 came to €81.6m for the year (€9.5m for the Housing division) compared with €28.3m in 2022. The €55m increase in the Boat division’s working capital requirements is linked primarily to the reduced level of client deposits (-€48m) resulting from the normalization of the order book. The Boat division’s €72m of net investments is €14m higher than the previous year, linked in particular to the measures rolled out to increase the flexibility of production capacity (+€10m) and improve the environmental impact of the buildings (+€3m).

Alongside this, the changes in scope represented a net investment of €13m. The Group acquired a controlling interest in the Tunisian-based yard Magic Yacht, in which it was a minority shareholder, as well as Wiziboat, a European digital boat club specialist. It also further strengthened its stake in Your Boat Club in the United States (from 40% to 49%) and acquired a 20% interest in YachtSolutions, specialized in supporting owner clients to create custom fit-outs for large units.

After dividend payments and share buybacks for €40m, net cash represented €247m at December 31, 2023, up €36m over the year.

The Group’s robust financial position is also illustrated by the €856m increase in its shareholders’ equity at December 31, 2023, compared with €706m at December 31, 2022.

Lastly, the return on capital employed (ROCE1) continued to progress in 2023 to reach 42% at the end of the year (versus 32% at December 31, 2022 and 14% at August 31, 2019). With revenues three times higher than the capital employed (stable between 2022 and 2023), and strong progress with the operating margin, this performance reflects the efficiency and effectiveness of the Group’s value-driven growth strategy.

SUSTAINABLE AND ACCESSIBLE BOATING

Strong progress across the three pillars from the B-Sustainable program, in line with the Group’s ambition for 2030

Groupe Beneteau ramped up the rollout of its B-Sustainable program, which was launched in 2022. The continued dedication shown by all of the teams made it possible to achieve sustained progress with all three pillars from this initiative.

Illustrating this, the CO2 emission intensity relating to electricity and gas consumption (scopes 1&2) came in 6% lower than 2022, the Boat division accident frequency rate was reduced by more than 9% over the period, and 41% of the Boat division’s purchases are now placed with suppliers whose CSR approach has been formally assessed (+17pts vs. 2022).

Moreover, after carrying out life cycle assessments on its main products, the Boat division was able to assess its first carbon footprint covering scope 3, helping set out concrete milestones for the next steps with its program to reduce its carbon intensity by -30% by 2030.

This program is based on continuing to move forward with the industrialization of innovative solutions, through the choice of materials used, integrating biosourced and recyclable elements, as well as the selection of alternative propulsion solutions and the optimization of its boat architecture solutions.

In line with this proactive approach, the Group acquired a stake in the Swedish company Candela, specialized in developing foiling electric boats. This technology aims to reduce energy consumption by 80%, while offering increased stability on the water and doubling or tripling the range levels achieved compared with other electric propulsion solutions. This minority interest will help drive the industrialization of decarbonized solutions for the recreational boat and passenger transport market.

New boating solutions: sharing economy and digital acceleration

Seanapps, Groupe Beneteau’s digital solution which connects end customers with their dealer and brand each day, is already fitted on around 8,000 boats. This connected fleet has already covered nearly one million nautical miles, making it the world’s most widely-established connected fleet by some distance. Feeding into a groundbreaking database, this app will enable the product teams to develop the next models, while ensuring close alignment with their clients’ usage practices.

During the year, the Group also further strengthened its positioning on various activities relating to the sharing economy. Thanks to the development of Your Boat Club’s activity in the United States and the acquisition of Wiziboat in Europe, the Group will now operate a fleet of over 500 boats, spread across around 50 bases. It expects to see double-digit business growth in 2024.

The weekly charter companies in which the Group acquired interests in 2021 returned to their pre-Covid levels of business from 2023 and now represent a fleet of over 1,000 boats. They will continue to turn around their profitability in 2024.

OUTLOOK

While the various premium segments continue to see very sustained levels of demand, the changes in interest rates are causing certain recreational boat owners to adopt a wait-and-see approach and encouraging dealers to scale back their stock coverage in 2024. As announced previously, the Group expects to see dealer inventory levels contract by around €100m to €150m in 2024, while 2023 benefited from a reverse phenomenon for around €240m, linked to the normalization of sourcing conditions.

Despite the scale of these differences in activity levels, the many different flexibility measures already anticipated, such as the adjustment of working times at certain French sites, will enable the Boat division to maintain an ordinary operating margin of 7% to 10% in 2024. While these significant variations in inventory levels are expected to be canceled out in 2025, the growth drivers put in place and the further structural efficiency gains to be rolled out will enable the Group to return to a double-digit operating margin within this timeframe.