The Global Yachting Market 2026: market normalises, but Italy continues to gain market share

Milan – A market slowing in volume but growing in value, an Italy continuing to expand its global market share, and a profound transformation of the marine industry, increasingly less linked to simple boat ownership and more oriented towards experience, services and technology. These were among the key themes emerging from the fourth edition of “The State of the Global Yachting Market”, the study prepared by Deloitte for Confindustria Nautica and presented this morning at Palazzo Mezzanotte, headquarters of Borsa Italiana.

The event, attended by PressMare, opened with remarks from Roberta La Veneziana of Borsa Italiana, who highlighted the role of capital markets as a strategic lever for business growth, describing stock market listing not only as a financial instrument but also as a driver supporting innovation, internationalisation and industrial development. Her speech also addressed the ongoing regulatory process at both European and Italian level aimed at simplifying companies’ access to financial markets through measures such as the European Listing Act, the Italian Capital Law and the recent reform of the Consolidated Finance Act (TUF).

Marina Stella, General Manager of Confindustria Nautica, noted that the relationship with Borsa Italiana has now become a well-established annual meeting point for industry, finance and sector stakeholders, underlining the strategic importance of data at a time marked by geopolitical instability and continuous changes in key markets. Stella emphasised how the premium superyacht segment continues to demonstrate solid fundamentals and the ability to maintain global industrial leadership, contributing significantly to Italy’s trade surplus.

Opening the economic analysis was Stefano Pagani Isnardi, Head of Research at Confindustria Nautica, who recalled that the Italian sector reached a record turnover of €8.6 billion in 2024. The national marine industry also confirmed its strong international vocation, with exports accounting for around 90% of domestic new-build production.

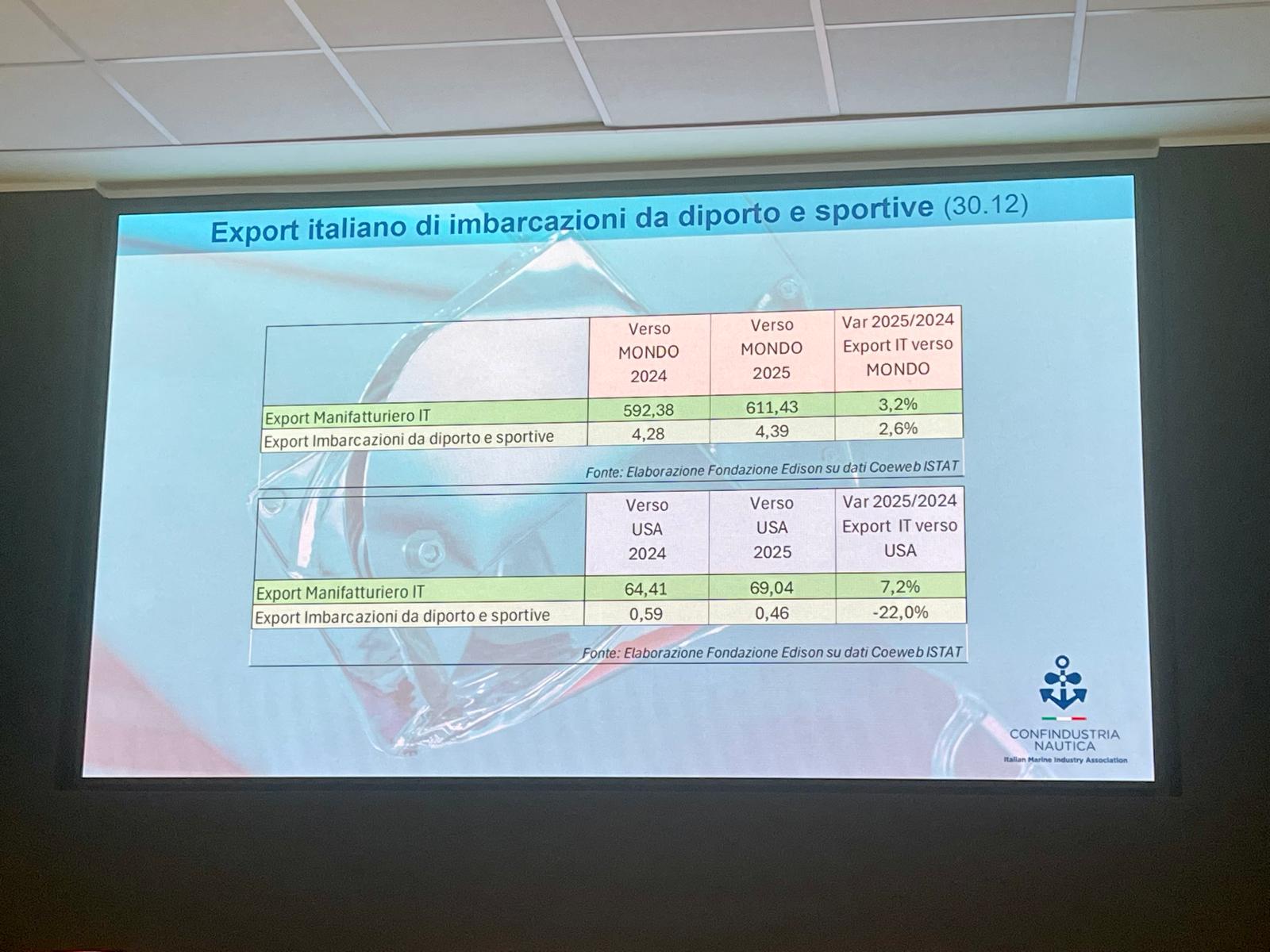

Preliminary figures prepared by Fondazione Edison show that in 2025 Italian marine exports reached a new all-time high, approaching €4.4 billion, up 2.6%, with peaks exceeding €4.5 billion during the year. Within this framework, however, a new element has emerged compared with recent years: the slowdown in trade with the United States, historically the leading destination market for the Italian industry, which recorded a 22% contraction. According to the conference speakers, one of the main reasons lies in uncertainty surrounding US tariff policies.

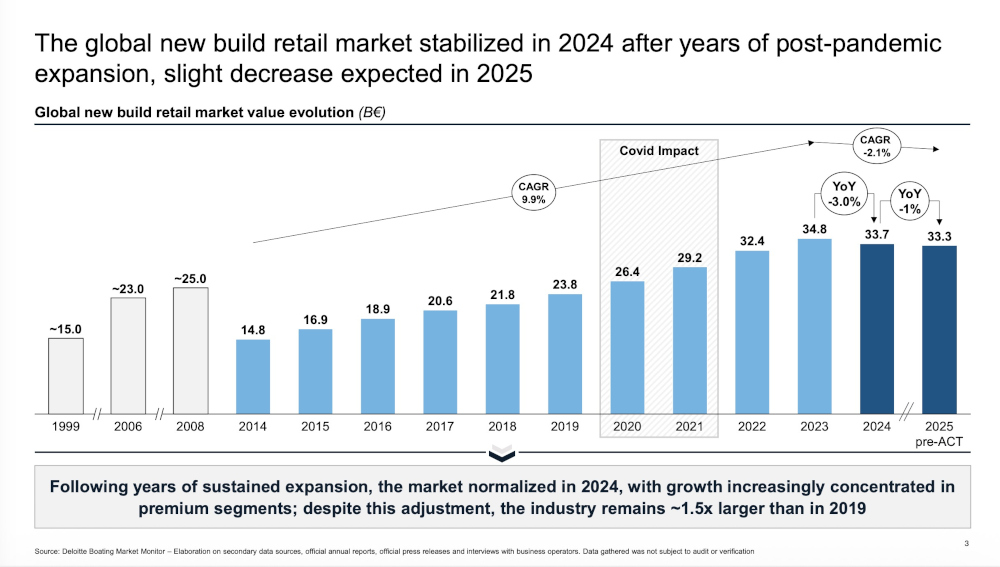

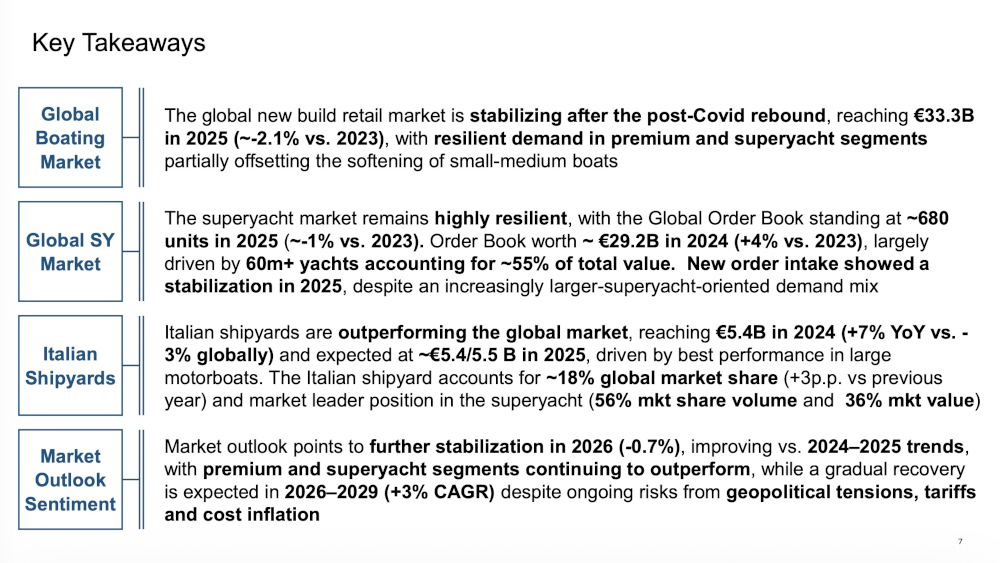

The Deloitte analysis, presented by Tommaso Nastasi, Deloitte Strategy & Value Creation Leader, showed that the global new boat market is undergoing a normalisation phase after the post-pandemic expansion. In 2025, the global market value is estimated at around €33 billion, with an average contraction of 2% over the 2023–2025 period. However, compared with 2019, the market still remains approximately one and a half times larger than in the pre-Covid period, a factor that, according to Deloitte, confirms much stronger fundamentals than in the past.

This normalisation is not affecting all segments equally. The inboard and premium boating sectors are proving more resilient. In 2024, while the global market declined by 3%, the inboard segment grew by 2%, whereas small boats, outboards and RIBs (-11%) and sailing yachts (-3%) were more heavily affected. The trend continued in 2025, with the inboard sector still growing, albeit moderately, while smaller recreational boating remained under pressure.

North America remains the world’s leading market, accounting for approximately 50% of the total, followed by Europe with 25%, while the rest of the world represents roughly a quarter of the global market. The European market is characterised by a stronger presence of inboard boats and sailing yachts, a segment in which Europe continues to hold a leading global position.

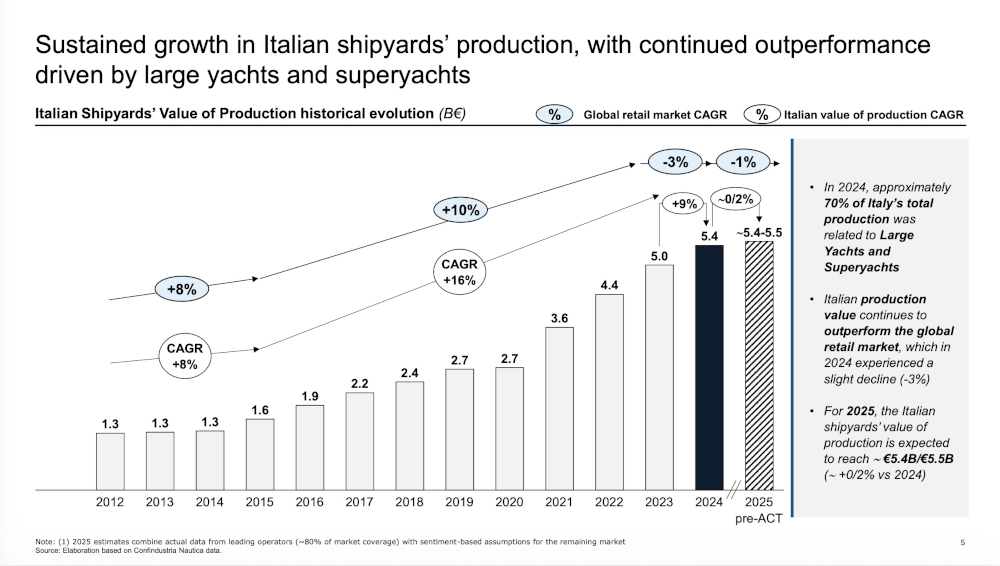

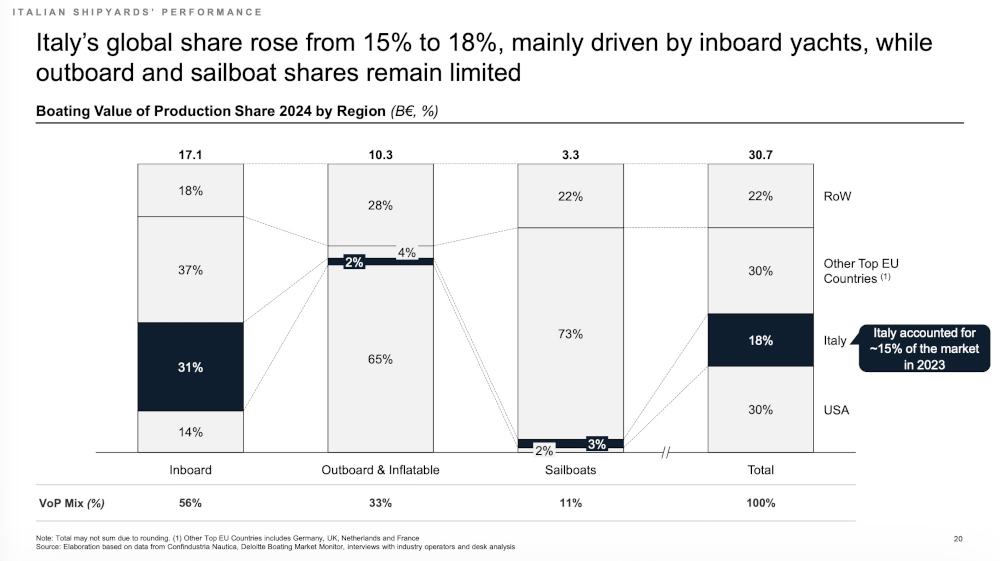

Within this context, Italy continues to stand out with performance above the international average. In 2024, the Italian marine industry grew by 9%, against a global contraction of 3%, while Deloitte estimates growth between 0% and 2% for 2025, still outperforming the global market trend.

One of the key factors behind Italy’s competitiveness is its production specialisation. Around 95% of the national industrial structure is concentrated in the inboard segment, compared with a global average of 60%. Italian production in this segment grew by 10%, compared with much more limited growth worldwide. According to Deloitte, this focus on mid-high and premium yachts has enabled the Italian industry to absorb macroeconomic turbulence more effectively.

In terms of market share, Italy further strengthened its leadership. The country’s share of the global market rose from 15% to 18% in just one year, while in the inboard segment alone the share reached 31%. Even stronger is Italy’s position in the superyacht sector over 30 metres, where the country holds 56% of the global market by volume and 36% by value, up from 34% the previous year. Italy is particularly dominant in the 30-to-60-metre range, where it controls around 60% of the global market.

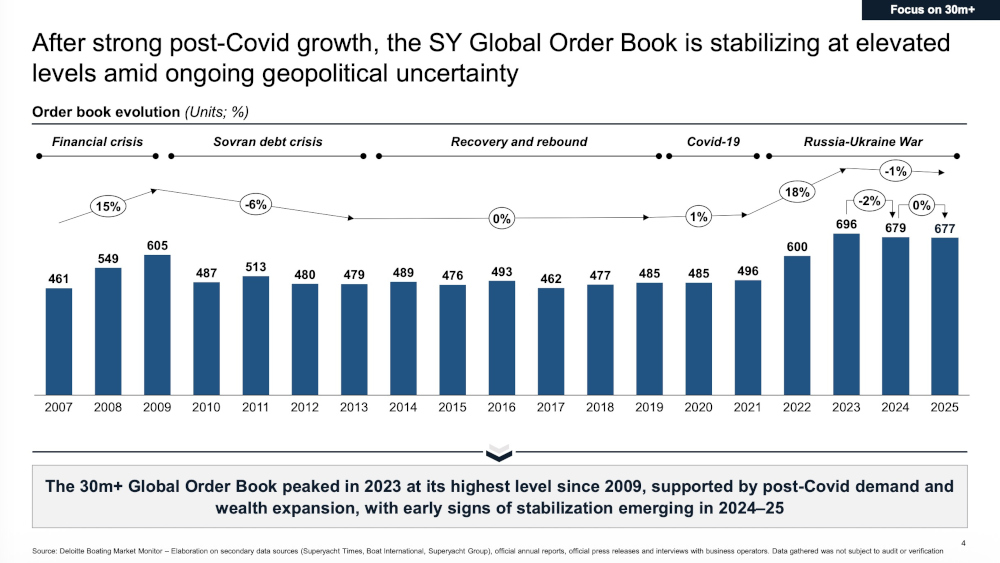

The superyacht market continues to represent the strongest and most strategic segment of the entire global yachting industry. The global order book remains around 700 units, compared with approximately 500 in the pre-pandemic period, with a total value close to €30 billion. In addition, yachts over 60 metres now account for approximately 55% of the total value of the global order book.

According to Nastasi, the market is increasingly moving towards larger, more complex yachts with higher technological and design content. This trend also emerges from new-order analysis, where the share of yachts between 40 and 60 metres and steel-built units is increasing. Within this framework, Italy continues to show superior capability compared with international competitors in securing new orders.

Looking ahead, Deloitte forecasts a further adjustment phase in 2026, with a slight contraction of 0.7%, followed by a recovery between 2027 and 2029, with average growth of 3%. The future market, however, is expected to differ from the past: fewer volumes but higher value. Industry operators interviewed expect demand to focus increasingly on larger, technologically advanced yachts with stronger experiential content.

Among the main challenges identified are geopolitical tensions, customs duties and currency volatility, particularly regarding the US dollar. On the demand side, the growing influence of a new generation of owners is emerging, younger and with different expectations compared with previous generations. According to Deloitte, 30–40% of new orders for large yachts now come from younger clients, less interested in status symbols and more focused on design, onboard experience, connectivity and lifestyle aspects.

This shift is also influencing the industry’s business model. Attention towards integrated services, after-sales support, marinas, refit, storage and new ownership models is increasing. According to Deloitte, the future of yachting will see ever closer integration between product and services, alongside a growing role for artificial intelligence, hybrid technologies and connected boats. At the same time, the industry is expected to undergo a phase of industrial consolidation through M&A operations and greater integration across the supply chain.

In conclusion, the picture emerging from Palazzo Mezzanotte portrays a sector which, despite entering a more mature phase after the exceptional post-pandemic years, continues to display solid fundamentals. Within this scenario, the Italian industry — especially in the premium and superyacht segments — confirms its central role on the global stage, supported by exports, production specialisation, design capability and the progressive strengthening of industrial value and yachting-related services.

©PressMare - All rights reserved